by admin | Dec 5, 2025 | My Journey

4 Powerful Lessons on Rebuilding Your Life from Zero Introduction: When Your Whole World Vanishes Imagine waking up one day to find that the future you had meticulously planned, the security, the stability, the life you’d built with someone else, has disappeared. This...

by Loraine Marshall | Mar 3, 2025 | Mindset

Imagine waking up one day to find that the future you’d planned—the security, the stability, the dreams you’d built with someone else—has vanished. For me, this wasn’t just a thought experiment; it was my reality. After 11 years of trusting my partner and the promise...

by Loraine Marshall | Jul 8, 2024 | Success

Also Known As The Spiritual Law Of Success. The Laws of Success: Insights from Napoleon Hill, Catherine Ponder, and Randy Gage Success, in its many forms, has been a subject of fascination for centuries. While strategies and tactics may differ, many personal...

by Loraine Marshall | Jun 3, 2024 | Money

How to Release Your Money Blocks Understanding Money Blocks Have you ever felt a pang of guilt after buying a coffee, a knot of anxiety when checking your bank account, or a nagging fear when considering a raise? These are all signs of hidden money blocks – limiting...

by Loraine Marshall | May 14, 2024 | Money

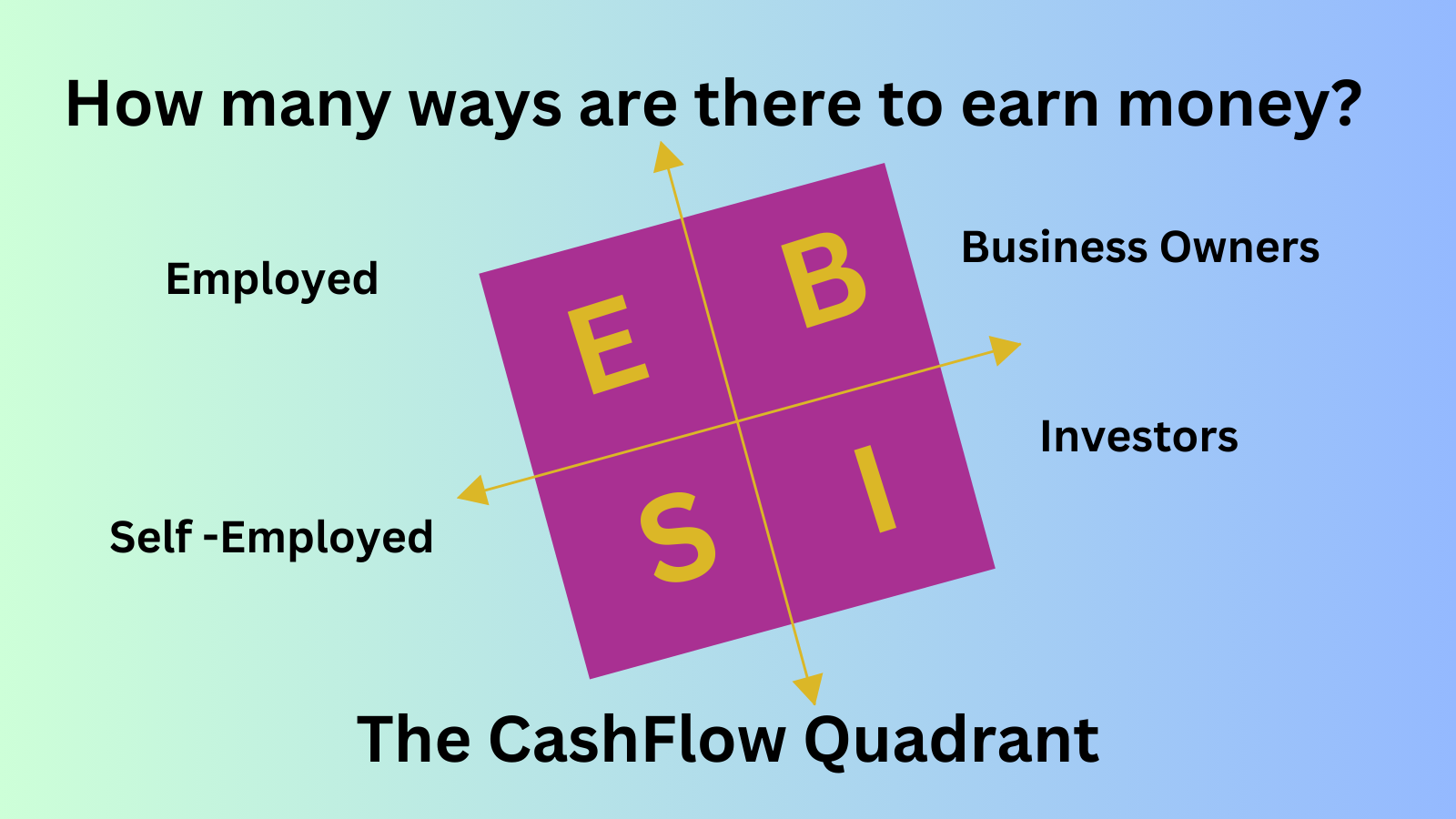

With the current economy in the doldrums, with weak economic growth, stubborn inflation and rising interest rates, the traditional ways of earning money have evolved into a diverse landscape filled with endless possibilities. From the conventional nine-to-five job to...

Recent Comments